Why Haven’t Loan Officers Been Told These Facts?

Regulation Z Steering Safe Harbor

Regulation Z 12 CFR §1026.36(e)(2-4)

(Paraphrased) A transaction does not violate the steering prohibition if the lender presents the consumer with appropriate loan options for each type of financing in which the consumer expresses an interest.

The loan originator must obtain loan options from a significant number of the creditors with which the originator regularly does business and, for each type of transaction in which the consumer expressed an interest . . .

Mortgage brokers can guard against steering violations by following Regulation Z’s steering safe harbor rules.

A transaction does not violate the steering prohibition if the lender presents the consumer with appropriate loan options for each type of financing in which the consumer expressed an interest.

For the safe harbor, Regulation Z enumerates these three types of financing

- A loan that has an annual percentage rate that cannot increase after consummation, such as a fixed-rate mortgage.

- A loan that has an annual percentage rate that may increase after consummation, such as a 5/1 ARM

- A reverse mortgage

Good steering and bad steering

The MLO must detail three financing examples for each type of financing the prospect is interested in. For example, the prospect considers a 5/1 ARM and a 30-year fixed rate. Those are two types of financing. The MLO then generates a comparison as follows.

30 year 5/1 ARM (A loan that has an annual percentage rate that may increase after consummation)

- Loan with the lowest rate with no riskier features

- Loan with the lowest fees

- Loan with the lowest rate

30 year fixed rate (A loan has an annual percentage rate that cannot increase after consummation)

- Loan with the lowest rate with no riskier features

- Loan with the lowest fees

- Loan with the lowest rate

In the example, generally, Regulation Z would require six discrete illustrations. Unfortunately, Regulation Z is silent about the format or detail necessary to satisfy the safe harbor provision. One might assume that a standard fee sheet comparison is sufficient.

For each type of transaction, if the originator presents more than three loans to the consumer, the originator must highlight the loans that satisfy the criteria, the lowest rate without riskier features, the lowest rate, and the lowest fees.

However, the loan originator can present fewer than three loans if the loans presented to the consumer satisfy the safe harbor criteria, e.g., the loan with the lowest rate also has no risky features.

1) The loan with the lowest interest rate and no riskier features means a loan without any of the following attributes:

- Negative amortization

- Prepayment penalty

- Interest-only payments

- A balloon payment in the first seven years of the life of the loan

- A demand feature (the loan is callable without preconditions)

- Shared equity

- Shared appreciation

2) The loan with the lowest total dollar amount of discount points, origination points, or origination fees. Primarily, the lowest fees apply to fees found on the Loan Estimate, Subheading A “Origination Charges” of the Loan Costs, Closing Costs Details.

3) The loan with the lowest interest rate is the lowest rate the consumer can likely obtain, regardless of how many discount points, origination points, or origination fees the consumer must pay.

For a loan that has an annual percentage rate that may increase after consummation, to identify the loan with the lowest interest rate, the MLO may consider the following loan types:

- For any loan that has an initial rate that is fixed for at least five years, the loan originator uses the initial rate that would be in effect at consummation.

- If the interest rate varies based on changes to an index and is subject to rate changes within the first five years, the originator uses the fully-indexed rate that would be in effect at consummation without regard to any initial discount or premium.

- For a step-rate loan, the originator uses the highest rate that would apply during the first five years.

It’s baseball season! Learn about improving your prospect conversions by throwing the Meatball pitch here: https://www.loanofficerschool.com/los-journal-volume-2-issue-4/

And don’t forget, the Loan Officer School’s 2022 CE tackles Regulation Z safe harbor challenges head-on in a simple hands-on presentation.

Behind the Scenes

Behind the Scenes

FHLMC’s three-year plan to address the needs of underserved communities.

Window Dressing or Substance?

ON THE SURFACE, BOLDER OBJECTIVES THAN FNMA’s THREE-YEAR PLAN

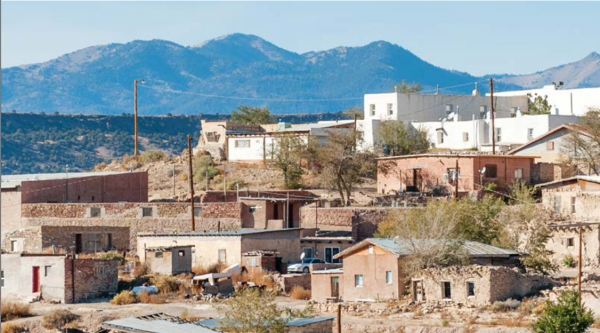

According to the 2010 U.S. Census, 42 percent of homes in rural areas were owned “free and clear” versus only 27 percent in urban and suburban areas. This may be in part because homes are less expensive overall or because older populations may have had more time to pay off mortgages or transfer equity from another property. However, there remains an overall need to provide affordable housing due, in part, to poor economic conditions. These economic conditions, in turn, can lead to borrowers with poor credit histories who lack available assets for down payments.

Freddie Mac offers a variety of loan products that support rural borrowers. Freddie Mac’s Home Possible® product provides flexible underwriting and low down-payment requirements, allows borrowers to obtain their down-payment funds from a variety of sources, and permits total loan-to-value ratios up to 105 percent. Home Possible can also be combined with a USDA Section 502 single-family leveraged second loan, which can be beneficial to rural households. Our HFA Advantage® is an extension of Home Possible and includes affordable product features with additional flexibilities for housing finance agencies. Additionally, we recently offered guidance to assist with rural property valuations. We recognize, however, that more work remains to be done.

Freddie Mac Duty to Serve Underserved Markets Plan 2022-2024 projected volume does not take into account potential market reactions to the interest-rate environment or the coronavirus pandemic. It also does not take into account the possibility of slower-than-expected adoption of our product enhancements. Lenders’ business priorities and the complexities of their internal processes affect the rate of adopting new or updated mortgage offerings.

CURRENT CHALLENGES

Rural borrowers have access to fewer mortgage lenders. Given the relatively low volume of loans and comparatively low home values in rural areas, it is less profitable for lenders to provide financial services in these areas. In addition, rural borrowers may not have access to reliable, consistent internet service. As a result, these borrowers may be completely reliant on one or two local lenders, who may have limited loan products and charge higher rates in order to maintain a local presence.

Rural appraisals are challenging for a number of reasons: there are limited comparable sales; those sales may not be similar to the subject property; and those sales may not be physically near the property being appraised. As a result, rural appraisals may take additional time, research and justification to determine an acceptable value for a property. Because of the additional work involved, rural appraisals may also cost more, an expense that is proportionately greater where the property value may be low.

Freddie Mac Duty to Serve Underserved Markets Plan 2022-2024 In addition, some economic opportunities may not extend to rural areas to the level that they are available elsewhere. Exacerbating these circumstances, the coronavirus pandemic has been causing unemployment and underemployment to rise, primarily in service-related industries. As a result, many potential homebuyers may remain on the sidelines and homeowners may be challenged to stay in their homes and/or holding off on investing in home improvements.

Furthermore, high-needs rural regions are primarily served by small community-based lenders; many may not have the capacity to sell directly to Freddie Mac and building relationships with aggregators through which they could deliver their loans takes time.

PROSPECTIVE PROVIDERS

Community Development Financial Institutions (CDFIs), minority depository institutions (MDIs) and smaller regional banks or small financial institutions (SFIs) have a unique place in the market. These institutions often have specialty programs and a great level of expertise with programs and financing directed towards the hardest-to-serve areas in their states and communities.

We estimate that we will provide lenders with an average of more than $2 billion in liquidity each year of this Plan cycle to finance homes in high-needs rural regions. Lenders originating the loans that we purchase may include CDFIs and small financial institutions; our purchases from rural areas will include loans securing manufactured homes, an affordable housing option for many households that tends to be more prevalent in rural regions than in other areas. Our loan purchases will expand access to credit to qualified borrowers and help create affordable homeownership opportunities in high-needs rural regions.

Keep an eye out for evolving opportunities

Partnering with local stakeholders might be a good place to start. Manufactured housing and other initiatives targeting entry-level homeownership opportunities might begin to gain support as the economy cools and the mortgage market continues to contract.

You can depend on two things in a tough market; mortgage lenders’ ever-increasing risk appetite and leaner profit margins. That makes yesterday’s less attractive lending opportunities shine more brightly. Lenders and other stakeholders will hit the drawing board to revise lending and housing objectives in light of the developing market conditions. Watch for emerging opportunities in manufactured housing.

Tip of the Week – Language Helps

Establishing yourself with non-native English-speaking communities may not be as out of reach as you might think. With the help of various stakeholders like the CFPB, FHFA, FNMA, and FHLMC, more and more non-English artifacts are available to help you help your customers better understand mortgage manufacture.

Providing appropriate disclosure as to the limits of ELP aids is a must. The FHFA Language Translation Disclosure is numero uno if providing non-English translations: https://www.fhfa.gov/MortgageTranslations/Pages/disclosure.aspx

Check out the FHFA library of language helps: https://www.fhfa.gov/MortgageTranslations/Pages/Search.aspx

Many loan artifacts in Spanish: https://www.consumerfinance.gov/about-us/blog/support-spanish-speaking-customers-with-spanish-language-disclosures/